According to the Budget speech of the Finance Minister, no income tax shall be payable up to income of Rs. 12 lakhs (after considering the rebate under section 87A). For the Assessment Year (AY) 2026-27, the Section 87A rebate remains unchanged under the Old Tax Regime, allowing individuals with a total income of up to ₹5 lakh to receive a 100% tax rebate, capped at ₹12,500.

However, under the New Tax Regime, the rebate has been significantly increased. In AY 2025-26, taxpayers with income up to ₹7 lakh were eligible for a rebate of ₹25,000, ensuring they paid no tax. For FY 2025-26 or (AY 2026-27), this rebate has been substantially enhanced to ₹60,000, benefiting individuals with income up to ₹12 lakh.

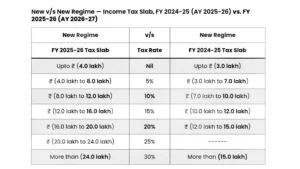

Key Tax Benefits Under the New Tax Regime (FY 2025-26)

This change under the New Tax Regime provides considerable relief to middle-income earners, reducing their tax burden and making the new regime more attractive. Meanwhile, the Old Tax Regime continues to offer stability with deductions and exemptions, but without any increase in the rebate limit.

Increased Tax Rebate (Section 87A):

- The tax rebate has been raised from ₹25,000 to ₹60,000.

- This benefits individuals with taxable income up to ₹12 lakh, compared to ₹7 lakh previously.

Standard Deduction for Salaried Individuals:

- A flat deduction of ₹75,000 is available on salary income.

- No supporting documents are required to claim this deduction.

- There is no change in the standard deduction limit for FY 2025-26.

NPS Contribution Deduction (Section 80CCD(2)):

- Employees can claim a deduction on their employer’s NPS contribution.

- Deduction limit: Up to 14% of Basic Pay + Dearness Allowance (for government employees) and 10% for private-sector employees.

- Example: If an employee’s basic salary is ₹10 lakh per annum, and their employer contributes ₹1.4 lakh to NPS, this amount is deducted from taxable income.

Tax-Free Income Up to ₹12 Lakh:

- A combination of the standard deduction and NPS employer contribution can bring taxable income down to ₹12 lakh.

- With the new ₹60,000 rebate, the individual will pay zero tax.

Tax on Excess Contributions to Retirement Funds:

- If an employer’s combined contributions to NPS, EPF, and superannuation fund exceed ₹7.5 lakh in a year, the excess amount is taxable.

- Any returns earned on the excess contribution will also be taxable.

- These provisions offer significant tax savings under the new regime while ensuring compliance with contribution limits.