How to Calculate Age in Google Sheets: 8 Effective Methods

Among the most effective formulas are DATEDIF, which quickly finds the difference between two dates, and YEARFRAC, which provides age in a decimal format.

Among the most effective formulas are DATEDIF, which quickly finds the difference between two dates, and YEARFRAC, which provides age in a decimal format.

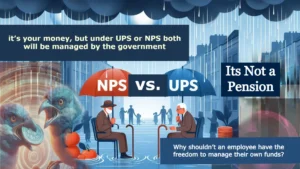

We compare the financial outcomes of the Unified Pension Scheme (UPS) and the National Pension System (NPS) for two employees, A and B, who share the same date of birth and retire after 25 years of service. Employee A opts for UPS, while Employee B chooses NPS.

You can easily auto-fill outer of LTC by selecting their Employee ID from a dropdown list, streamlining the process.

The National Pension System (NPS) allows employees to invest their retirement savings in various pension fund schemes managed by 11 fund managers, including SBI, LIC, and ICICI. Regulated by PFRDA, it offers investment flexibility across equities, government securities, and bonds.

Employee A, an ex-serviceman, retires at 60 under UPS, receiving a pension. Employee B, retiring at 42 under NPS, withdraws 60%, invests in FD, and gets an annuity. Employee C, retiring at 42 under UPS, waits until 60 for pension payouts

Under the UPS, the pension begins only after reaching the superannuation age (60 years). For the first 12 years after retirement, you do not receive any pension under the UPS scheme.

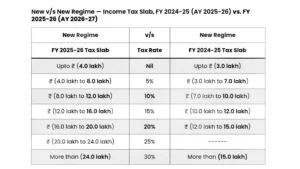

For AY 2026-27, the Old Tax Regime's Section 87A rebate remains ₹12,500 for incomes up to ₹5 lakh, while the New Tax Regime increases the rebate to ₹60,000 for incomes up to ₹12 lakh, reducing tax burdens.

FM announced that no income tax will be payable for annual income upto ₹12 lakh. Limit for tax deduction on interest income to be doubled to Rs 1 lakh for senior citizens.

NPS (with FD interest) offers greater financial security and wealth accumulation, while UPS provides a guaranteed pension but lacks the wealth-building potential and flexibility that NPS provides.

The Individual Corpus determines a UPS subscriber’s actual retirement savings, while the Benchmark Corpus serves as a reference standard set by the authority to assess whether the individual’s accumulated corpus is sufficient for a sustainable pension.